- A sportsbook is the counterparty to every bet and bakes a 4-5% margin (the vig) into its odds; DraftKings Predictions routes orders to a peer-to-peer exchange that charges per-contract fees and takes no directional position.

- DraftKings Predictions launched December 19, 2025 as a CFTC-registered Introducing Broker and NFA member, available for event contracts in 38 states and sports contracts in 17 states including California, Texas and Florida.

- DraftKings acquired Railbird Technologies (announced October 22, 2025), a CFTC-designated contract market, giving it an in-house exchange branded DKeX rather than relying solely on third parties like CME Group.

- Federal CFTC oversight under the Commodity Exchange Act differs fundamentally from state-by-state gambling regulation, and the boundary is actively contested in court by multiple state attorneys general.

- Event contracts are not bets that pay odds; they are $0-to-$1 instruments you can buy or sell before resolution, but they still carry real risk of loss and are not financial advice.

The short answer

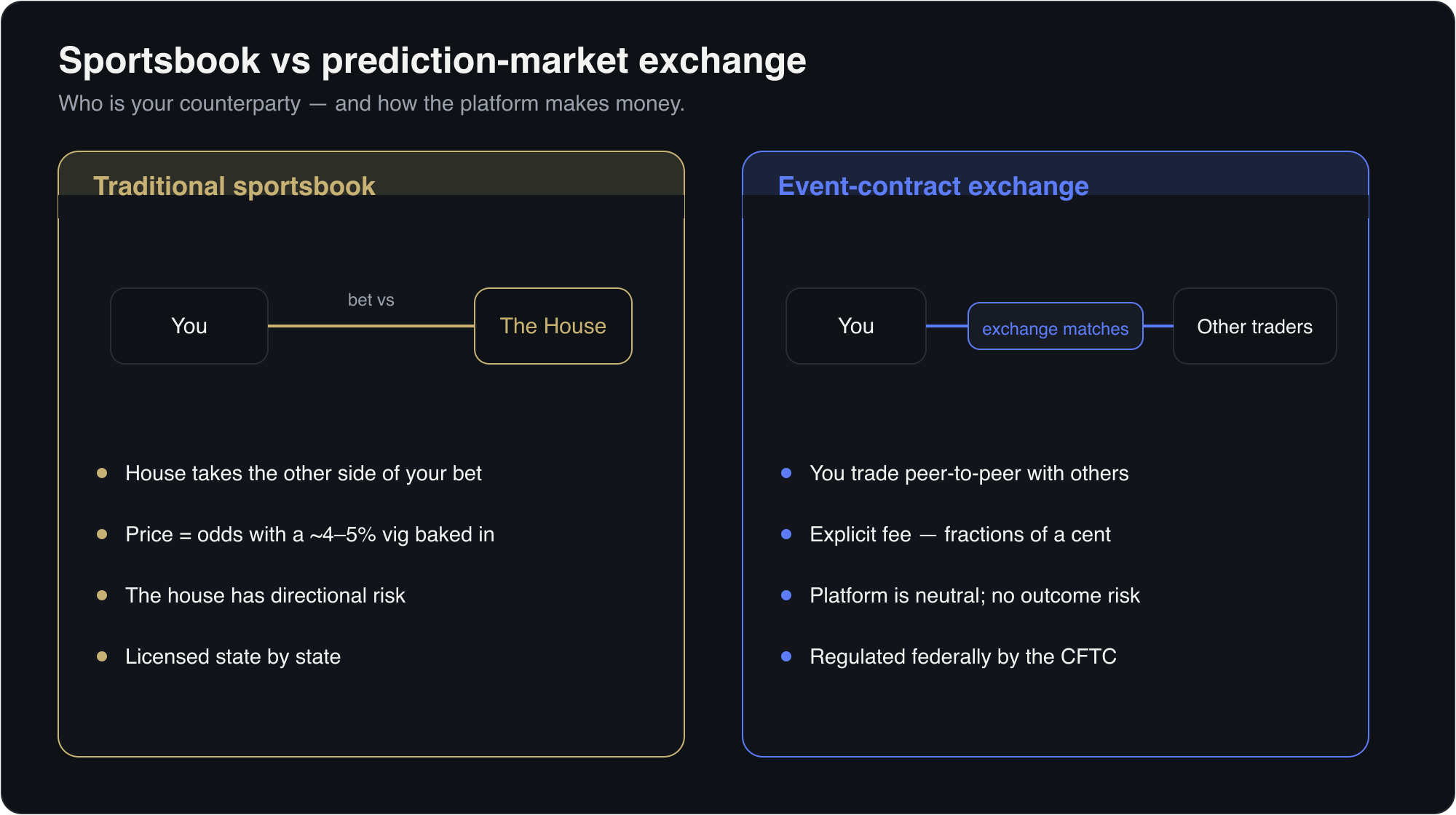

DraftKings Predictions and a traditional DraftKings sportsbook can look almost identical on screen, but they are different financial structures with different counterparties, different economics, and different regulators. A sportsbook is a house-banked operation: you bet against the book, the book sets the odds, and a built-in margin called the vig (typically 4–5%) is its revenue, per The Lines’ comparison. DraftKings Predictions is a front end to a CFTC-regulated event-contract exchange: you trade against other participants in an order book, the crowd sets the price, and the exchange earns a per-contract fee while taking no side. DraftKings launched the product on December 19, 2025 as a CFTC-registered introducing broker, available in 38 states (CoinDesk). The mechanics below explain why that distinction matters.

Risk note: Event contracts carry a real risk of loss, prices can move against you before resolution, and nothing here is financial or betting advice.

How a traditional sportsbook works

In a sportsbook, the operator is your counterparty on every wager. When DraftKings’ sportsbook offers the Chiefs at -110, it is not matching you with another bettor — it is taking the other side of your bet itself and managing its aggregate risk across all the action it accepts.

The vig (also called juice or the hold) is how this model makes money. Both sides of a two-way market are priced so the implied probabilities sum to more than 100%. At -110 on each side, a book is selling roughly $1.10 of risk to collect $1.00, embedding a hold of about 4–5% per market. The Lines describes the sportsbook structure plainly: “punters wager against the house regardless of who else is wagering,” with “odds calculated by the bookmaker (which include their profit margin and risk management).”

Two consequences follow:

- The book has directional exposure. If too much money lands on one side, the operator can lose. Books manage this by moving lines, capping limits, or laying off risk — but the house can be on the hook for outcomes.

- The book can subsidize. Because it expects to earn vig over time, a sportsbook can fund promos, boosted odds, and free bets from that future margin. There is a single, well-capitalized counterparty standing behind every position.

Crucially, sports betting is regulated state by state. The Lines notes sportsbooks are “regulated through state-level gambling licenses and local laws,” which is why DraftKings’ sportsbook is unavailable in states such as California and Texas.

How a prediction-market exchange works

A prediction market — also called an event-contract exchange — flips the structure. You are not betting against the house; you are trading a standardized contract with another participant, and the platform matches the two of you. As The Lines puts it, “participants trading directly with each other (peer-to-peer)” set “the prices based on crowd consensus.”

The instrument itself differs from a bet. Each contract has a nominal value of $1 and resolves to either $1 (the event happened) or $0 (it didn’t). You buy a “Yes” contract for some fraction of a dollar; if you pay $0.62 and the event resolves Yes, you collect $1.00. Because there is a live order book, you can also sell before resolution to lock in a gain or cut a loss — something a settled sportsbook ticket generally does not allow.

The economics are structurally different in three ways:

- The exchange is neutral. It earns a transaction fee per contract and holds no directional position, so it does not care which side wins. There is no “house” with exposure to the outcome.

- There is no embedded vig. Instead of a 4–5% margin baked into the odds, the platform charges an explicit fee. On DraftKings’ own exchange, public CFTC filings reported by DeFi Rate set taker fees at $0.005 to $0.01 per contract and maker fees at $0.0025 per contract — fractions of a cent, not several percent of stake.

- No single counterparty to subsidize you. Because the platform takes no margin on the outcome, there is no future vig pool to fund the kind of risk-free bets and odds boosts sportsbooks lean on.

Most consequentially, these exchanges are regulated federally by the Commodity Futures Trading Commission (CFTC) under the Commodity Exchange Act (CEA) — not by state gaming commissions. That single fact drives both DraftKings’ national reach and the litigation swirling around the category.

House book vs exchange: side by side

| Dimension | Traditional sportsbook | Prediction-market exchange (DraftKings Predictions) |

|---|---|---|

| Counterparty | The house (operator takes the other side) | Another participant; platform only matches |

| Who sets the price | The bookmaker | The order book / crowd consensus |

| How the platform earns | Vig embedded in odds (~4–5% hold) | Explicit per-contract fee (fractions of a cent on DKeX) |

| Directional risk | Operator can win or lose on outcomes | Platform is neutral; no outcome exposure |

| Instrument | Bet that pays at fixed odds | $0–$1 contract you can buy or sell pre-resolution |

| Exit before the event | Limited (cash-out, if offered) | Yes — trade out of the position in the book |

| Primary regulator | State gaming regulators | CFTC, under the Commodity Exchange Act |

| DraftKings status | State-licensed sportsbook operator | CFTC-registered Introducing Broker; NFA member |

Sources: The Lines, DeFi Rate, CoinDesk.

What DraftKings actually launched

DraftKings Predictions went live on December 19, 2025 as a standalone app and web product that, in DraftKings’ framing, “lets users trade on the outcomes of real-world events, starting with sports and finance,” with entertainment and culture planned later (CoinDesk).

The legal architecture is the headline. The product operates through a wholly owned DraftKings subsidiary registered with the CFTC as an Introducing Broker and a member of the National Futures Association, per Finance Magnates. That federal status is what lets DraftKings offer event contracts in 38 states — and, notably, sports event contracts in 17 of them, including California, Texas and Florida, where its traditional sportsbook cannot operate.

On the supply side, DraftKings is plugging into existing infrastructure first. At launch it “will connect to the CME Group,” giving access to “economic indicators, global benchmarks, and sports events,” with its own acquired exchange “expected to integrate… in the future” (Finance Magnates).

The Railbird acquisition and DKeX

DraftKings did not just license access to someone else’s exchange — it bought one. On October 22, 2025, DraftKings announced the acquisition of Railbird Technologies, a CFTC-authorized exchange; per John Lothian News, “the terms of the deal were not disclosed.”

Railbird’s pedigree explains the appeal:

- Founded in 2021 and a graduate of Y Combinator’s Winter 2022 batch; co-founder and CEO Miles Saffran was previously an investment research analyst at Point72 covering the fintech and gaming sectors (Y Combinator).

- Granted Designated Contract Market (DCM) status by the CFTC in June 2025 (PR Newswire), the same exchange license category Kalshi holds.

- Runs on the EP3 match engine from Connamara, per John Lothian News.

A DCM is the key asset. As PR Newswire describes it, the designation “permits the operation of a regulated futures exchange where users can trade derivative contracts based on real-world event outcomes.” Owning the DCM lets DraftKings list contracts on its own venue — branded DKeX (the Railbird Exchange, CFTC identifier “REX”) — and self-certify new products rather than depending entirely on third parties.

That machinery is now running. As of late May 2026, public CFTC filings reported by DeFi Rate show DKeX self-certified six sports contract templates — game winners, spreads, game/player properties, entity statistics, achievements, and head-to-head markets — spanning football, basketball, baseball, hockey, golf, MMA, motorsports, soccer and tennis, with contracts set to list after the close on May 27, 2026.

Why this is contested, not settled

The structural distinction is also a legal fault line, and any trader should understand that the regulatory ground is moving.

The advantage event-contract exchanges claim is federal preemption. Law firm Stinson LLP explains that as a DCM, an exchange is “allowed to create and offer ‘event contracts’ regulated by the Commodit[y] Exchange Act (CEA) and to self-certify that such contracts are compliant.” Federal courts in Nevada and New Jersey sided with this view, reasoning that because the operator is a DCM under the CEA, its contracts are “governed exclusively by the CEA.” But Stinson notes the Maryland court disagreed, holding the CEA’s preemptive effect “does not mean Congress intended… to encompass state gambling and sports wagering laws.”

The CEA also contains a gaming carve-out: the CFTC may “review and prohibit certain types of event contracts that are contrary to the public interest, including those related to gaming,” per Stinson LLP. Whether sports contracts fall inside that carve-out is the unresolved question.

The stakes are concrete. On the largest CFTC exchange, Kalshi, sports made up over 90% of activity and 89% of revenue ($263.5 million) in 2025, per Wikipedia’s Kalshi entry. That has triggered a wave of state attorney-general lawsuits — Massachusetts (September 2025), New York (November 2025), and Michigan, Nevada, Arizona, Washington and Wisconsin in early 2026 — with a Massachusetts judge granting a preliminary injunction in January 2026. DraftKings, entering the same arena, inherits the same exposure.

What it means for traders

If you trade DraftKings Predictions, treat it as an exchange, not a sportsbook:

- Price, don’t accept odds. You set limit prices and can sell before an event resolves. Fees are per contract, not a hidden percentage of stake — generally cheaper than vig at scale, but read the fee schedule.

- There’s no house to lean on. Liquidity comes from other traders, so thin markets can mean wide spreads and slippage.

- The legal status can change. A court ruling, a CFTC rulemaking, or new legislation could alter availability in your state. This is a developing space, not a settled one.

At MispriceHQ, our forthcoming machine-learning engine is being built to estimate fair value for these $0–$1 contracts and flag where market prices may diverge from it. To be explicit: that model is in development — it has no live track record and has not resolved markets. We will describe its methodology and performance only once it is validated.

Reminder: event contracts carry a real risk of loss; this article is informational and not financial or betting advice.

Frequently asked questions

Is DraftKings Predictions the same as the DraftKings sportsbook?

No. The sportsbook is a state-licensed, house-banked operation where you bet against DraftKings and the odds include its vig. DraftKings Predictions is a CFTC-regulated event-contract platform where you trade $0-to-$1 contracts peer-to-peer in an order book, and DraftKings earns a per-contract fee instead of taking the other side of your wager.

When did DraftKings launch its prediction markets and where is it available?

DraftKings Predictions launched on December 19, 2025, operating through a CFTC-registered Introducing Broker subsidiary that is also an NFA member. According to CoinDesk and Finance Magnates, event contracts are available in 38 states, with sports event contracts in 17 states, including California, Texas and Florida, where its traditional sportsbook cannot operate.

What is Railbird and why did DraftKings buy it?

Railbird Technologies is a CFTC-designated contract market (DCM) founded in 2021 by former Point72 analysts and a Y Combinator W2022 alum. It received CFTC DCM approval in June 2025. DraftKings announced the acquisition on October 22, 2025 (terms undisclosed) to gain its own exchange, branded DKeX, so it can list and self-certify contracts rather than relying only on third parties like CME Group.

What is the vig, and do prediction markets have it?

The vig (or hold) is the margin a sportsbook bakes into its odds, typically 4-5% per market, by pricing both sides so implied probabilities exceed 100%. Prediction-market exchanges do not embed a vig; they charge an explicit transaction fee instead. On DraftKings' DKeX, CFTC filings reported by DeFi Rate list taker fees of $0.005-$0.01 and maker fees of $0.0025 per contract.

Are CFTC-regulated sports event contracts legal everywhere?

It is contested. Operators argue the Commodity Exchange Act preempts state gambling law, and federal courts in Nevada and New Jersey agreed. But a Maryland court disagreed, and multiple state attorneys general have sued Kalshi, with a Massachusetts judge issuing a preliminary injunction in January 2026. The CFTC has signaled new rulemaking. Availability in a given state can change.

Can I sell a prediction-market position before the event ends?

Usually yes. Because contracts trade in a live order book and are priced between $0 and $1, you can buy or sell before resolution to lock in a gain or limit a loss, subject to liquidity. A settled sportsbook bet generally cannot be exited that way, aside from limited cash-out features some books offer. Thin markets can still produce wide spreads.

- DraftKings enters prediction markets with CFTC-approved app for real-world events — CoinDesk (2025-12-19)

- CFTC Oversight Sees DraftKings Launch Prediction Markets Through CME Group — Finance Magnates (2025-12-19)

- DraftKings Buys CFTC-Regulated Exchange in Prediction-Market Bet — John Lothian News (2025-10-22)

- Railbird Receives CFTC Approval as a Designated Contract Market — PR Newswire (Railbird) (2025-06-18)

- Railbird: A futures market for events — Y Combinator (2022)

- DraftKings Railbird Exchange Files First Sports Prediction Market Contracts — DeFi Rate (2026-05-26)

- Prediction Markets vs Sportsbooks 2026: Our Comparison — The Lines (2026)

- Sportsbooks or Commodity Exchanges? The Rising Legal Tensions Between Sports Betting and Prediction Markets — Stinson LLP (2025)

- Kalshi — Wikipedia (2026)

- Prediction Markets vs. Sports Betting: Similar Mechanics, Different Structures — Sports Illustrated (2026)